Home prices are heavily driven by the purchasing power of the buyer pool. From a macro-economic level, that means the job market, equity markets, and mortgage rates are the three primary contributors to the health of the housing market. Currently, the market is buzzing with talk about mortage rates following the Fed's lowering of the fed funds rate by 0.50% on September 18th. I will address some key points on interest rates, including the irony that mortgage rates did not decrease following the long-awaited September 18th fed funds rate decrease. In fact, September 17th, the day BEFORE the Fed dropped rates, had the lowest mortgage rates in all of 2024.

Why did mortgage rates NOT decline when the Fed reduced the fed funds rate on September 18th? Remember that the Fed sets the fed funds rate, which dictates short-term lending rates...think credit cards, auto loans, student loans, and home equity lines of credit. When the Fed implemented the 0.50% reduction on September 18th, this instantly impacted short-term lending rates, which had not moved prior to the Fed's announced rate decline. To the contrary, mortgage rates track longer-term bond markets. Typically the 10-year treasury is a good guide for movement in mortgage rates. The longer-term bond markets, including the 10 year treasury, are impacted by a variety of factors, including economic data and forecasts, buyer demand to purchase U.S. treasury notes, and geopolitical events. In this case, the long-term bond markets - and mortgage rates - started coming down in late July as the bond markets became increasingly confident that the Fed was actually going to kick off a series of rate drops. Since the Fed announced the rate reduction two weeks ago, rates have actually edged higher. This is counterintuitive on the surface, but a result of market fears of increased treasury bond supply as the government spends money (adds national debt) to support and aid Hurricane Helene relief and ongoing Middle East conflicts. If the government issues new bonds, that means the supply of bonds increases, and therefore buyers of the debt will require a higher interest rate in order to absorb/purchase the excessive debt, and push up the rates, which mortgage rates will track.

What is the outlook for mortgage rates for the rest of 2024? It is important to look at the shift in mortgage rates that began in late July and ran through September 17th. At this point, the market has full confidence in the Fed continuing to drop the fed funds rate at their two remaining meetings of 2024, and has already priced those into the long term bond pricing. Said differently, everything for 2024 is already baked into the cake. The Fed is expected to have another 0.50% drop in the fed funds rate for 2024, but this will not move mortgage rates further, all else being equal, since it is already fully priced in to what we are currently seeing. That means home buyers and sellers will see a pretty steady rate environment for the remainder of 2024. Home buyers and sellers should expect no benefit from "waiting for later Fed action" in 2024, since the bond markets and mortgage rates will not adjust, unless there is a surprise with the expected Fed cuts.

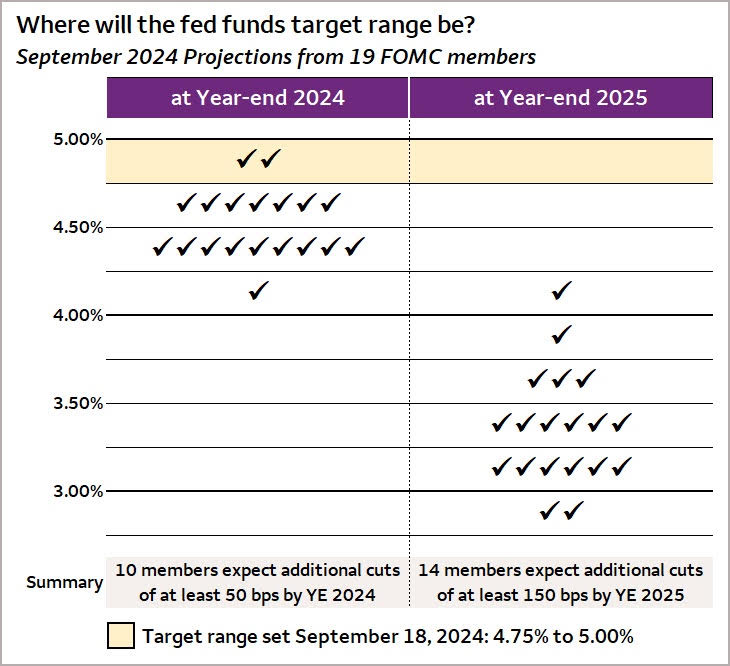

What could we expect in 2025? There is a consensus prediction that the Fed will have additional fed funds rate cuts in 2025, but there are varying opinions as to the extent of those cuts. While 2024 is "baked into the current cake", probabilities for 2025 are much more fluid, and mortgage rates should see additional drops if the Fed does in fact follow through with continued reductions in 2025. The chart below is a helpful guide to the distribution of forecasts for 2025, but the predominant expectation is a 1.00%+ drop beyond the 4.50% expected 2024 year-end rate.

Whether you're buying, selling, or investing, my goal is to ensure your experience is stress-free, successful, and guided by thoughtful planning. I am committed to helping you achieve the best possible outcome, with a focus on your unique needs and goals. This is best achieved with advanced planning, and an advisor by your side to help you navigate the dynamic and evolving market. Reach out to me at [email protected], and we will solidify your real estate vision and begin to formulate your optimal roadmap.